2024 Annual Review – Another “abnormally” strong year for investors

It was another impressive year for share market investors with calendar 2024 delivering average returns on global developed markets of just over 20%. This is the second consecutive year in which returns have been at this level, which is nearly 3 times the long-term annual average.

The primary driver of the abnormally high global equity market returns in 2024 continued to be the large US technology companies, which on average delivered growth of 56%. Underlying this growth has been the ongoing evolution of Artificial Intelligence related hardware and software, which has impacted positively on actual and forecast company earnings.

Much of the focus in the second half of 2024 was on the U.S. election. The clear-cut election result was viewed positively by equity markets, as it removed a source of uncertainty and set-up a reduction in U.S. corporate tax rates and deregulation initiatives. With the agenda of the new U.S. administration being overtly “America First”, U.S. domiciled companies and the U.S. dollar were clear beneficiaries of the election result.

However, notwithstanding the rally in November following the U.S. election, there was a slowing in overall equity market momentum in the second half of calendar 2024, with nearly two-thirds of the annual gain on global markets coming in the first 6 months of the year. The slowing in the momentum appeared to be related to the outlook for interest rates. With global economic growth stronger than expected, particularly in the U.S., there was a reassessment of the magnitude and pace of decline in inflation and future cash interest rates. Despite most developed economy central banks easing monetary policy and pushing cash interest rates lower, longer term bond yields increased over the course of 2024. The higher bond yields did subdue the equity market rally later in the year to some extent.

Although the U.S. election and the U.S. technology sector were key factors of support for share markets, some key non-U.S. markets kept pace with the broader average for most of the year. Compared with the 25.0% increase in the U.S. S&P 500 Index, share markets in Germany (up 18.6%) and Japan (up 20.9%) performed well. However, a weak economic backdrop did result in more muted performances in parts of Europe, with the United Kingdom (up 9.5%) also impacted by lower energy prices.

With an average return of 10.4%, share markets in emerging economies generated around half the growth of developed economy share markets. In contrast to recent years, the Chinese share market outperformed with a gain of 18.2%. A series of economic stimulus measures announced by Chinese authorities in the second half of the year did boost confidence in the Chinese market. In contrast, Korea (down 12.4%) and Brazil (down 11.7%) detracted from emerging market returns. Weaker commodity prices were a negative influence on various emerging markets, such as Brazil.

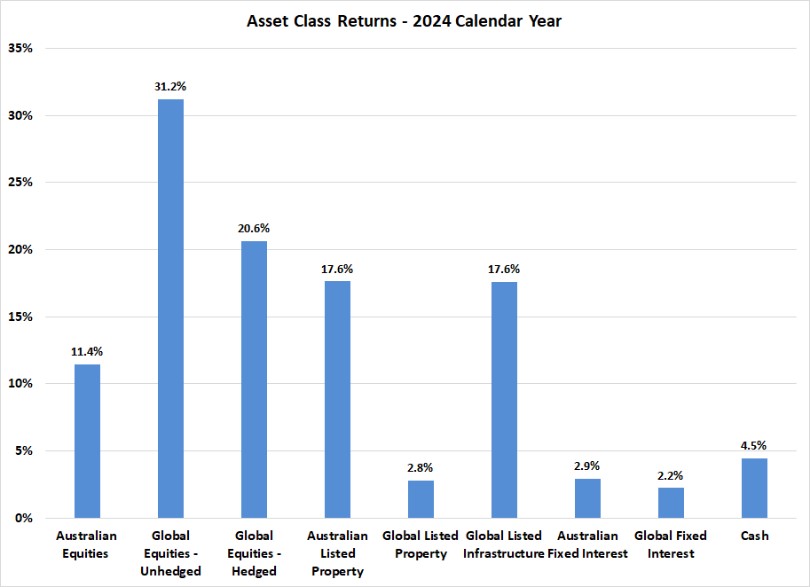

Despite some periods of strong support, listed property failed to keep pace with listed equities more generally. The global Real Estate Trust (REIT) sector finished the year just 2.8% higher. Australian REITs performed better with a 17.6% gain, primarily due to the largest constituent in the index, Goodman Group, rallying 42.1%. Goodman Group’s global data centre initiatives were a catalyst for attracting substantial investor interest, with the stock now making up more than 40% of the local AREIT Index. However, more broadly, listed property was weighed down by higher bond yields and concerns over office property. Infrastructure, however, was more broadly supported, in returning 17.6% for the year.

Like emerging markets, the Australian share market was also weighed down by lower commodity prices, with the S&P ASX 200 Index returning 11.4%. Resource and energy stocks declined by 14.9% and 13.9% respectively over 2024. Some sectors, such as financials (up 33.7%) attracted strong support, despite lofty valuations. Although the technology sector was the best performed, with an increase of 49.9%, the small size of this sector in Australia made it difficult for the local market to maintain the same trajectory as the U.S. market.

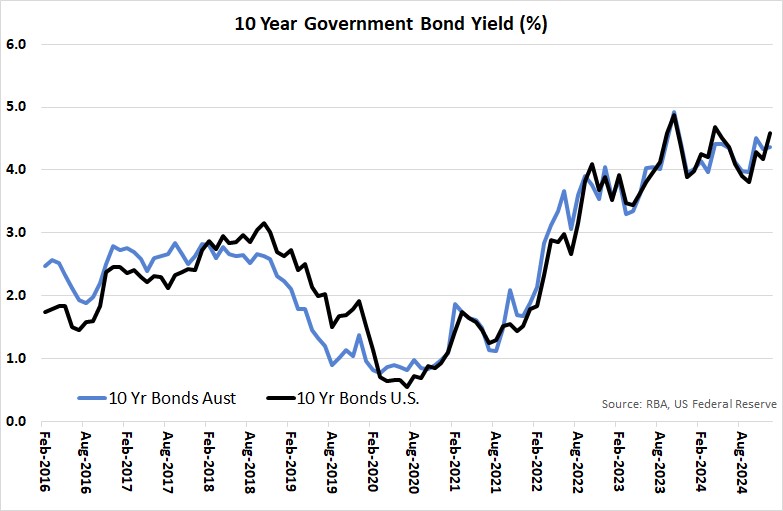

As was expected at the start of the year, cash interest rates declined around the globe as evidence of inflation pulling back from post-COVID highs enabled central banks to ease policy. However, with economic growth remaining stronger than expected, fewer cash rate reductions are now anticipated in 2025, and bond yields have shifted upwards to reflect this higher interest rate outlook. Over the course of 2024, the U.S. 10-year Treasury yield shifted from 3.88% to 4.58%.

Australia has been an exception to the broader trend, in that inflation here has proved stickier to date, thereby not providing the opportunity for the Reserve Bank to cut cash rates. However, with the underlying economy weak (eight out of the past nine quarters have produced negative economic growth on a per person basis), expectations for lower inflation and cash rate reductions in 2025 remain. With the economic outlook in Australia weaker, bond yields here did not increase to the same extent as the U.S., although the trend was still upwards with the 10-year Government bond yield finishing the year 0.41% higher at 4.37%. Higher bond yields led to lower bond prices, although fixed interest asset class returns were still positive for investors over 2024 due to the relatively high running yield received.

The election result and a higher interest rate outlook in the United States provided a source of strong support for the $US last year. As a result, the $A declined from U.S. 68.4 cents to U.S. 62.2 cents. The $A also declined 3.3% against the Euro but was a marginal 0.4% stronger against the Japanese Yen. With commodity prices remaining relatively soft and local interest rates expected to fall, there has been a decline in support for the $A over the past year. However, for investors with unhedged currency exposure attached to overseas investments, this was a source of significant gain throughout 2024.

Outlook and Portfolio Positioning

For much of 2024, financial markets across the globe were highly synchronised, with patterns in U.S. equity and bond markets being mimicked across other geographical markets. Towards the end of the year, however, trends were notably more disparate. In the month of December, for example, equities declined in the United States but increased in Japan and parts of Europe. Bond yields were steady in Australia, but sharply higher in the U.S. Within equity markets, investors retreated to defensive stocks in Australia, but continued to support most of the large technology stocks in the U.S.

Overall, there appeared to be a strong element of logic in the divergent movements across equity and bond markets in December. Potentially, the month is the commencement of a period where investors become more discerning over asset selection, with fundamentals playing a greater role than momentum and sentiment in determining performance. Perhaps, valuations have reached a level whereby the marginal investor is no longer willing to just “buy the market” and needs supportive fundamentals to justify further investment.

In fact, there is some evidence to suggest that the dominant market leadership provided by the US technology sector over recent years has been waning in influence. In the year to June 2024, the correlation of monthly returns between the technology heavy US NASDAQ Index (in local USD) and the Australian S&P ASX 200 Index was relatively high at 56%. By the end of 2024, this 12-month rolling correlation had dropped to just 5%.

Should directional performance across different geographical regions and sectors of equity markets continue to become less correlated, then opportunities for active managers to add value may be enhanced. Recent years have been difficult for active equity managers, as the direction of markets has been so heavily impacted by the Artificial Intelligence (AI) thematic and the price movement of the large U.S. technology stocks. Unless active managers have been prepared to take on larger positions in an increasingly expensive and less diversified mix of stocks at the mega cap end of the global equity index (which goes against the grain of many active managers’ risk aware philosophies), then performance is likely to have suffered relative to broader market benchmark measures.

Notwithstanding some relative underperformance from active managers, the last two calendar years on global equity markets have been abnormal in terms of the magnitude of return, with both 2023 and 2024 delivering returns in excess of 20%. Whilst a continuation of this level of return is unlikely, there remains cause for optimism given the favourable global economic backdrop, strong position of corporate balance sheets and the potential for AI to deliver yet to be recognised opportunities.

However, not all companies, sectors or geographies are well positioned to capitalise on these opportunities. Much of the Australian share market, for example, appears challenged to deliver the earnings growth assumed in current valuations – although Australian resource stocks are appearing increasingly undervalued compared with the broader asset class. Similarly, emerging markets and smaller companies still appear cheap relative to the equity market in general. As such, having an active portfolio management approach that is able to respond to changing fundamentals and valuations may be more important and rewarding in 2025 than it has been in recent years.

Important Information

The following indexes are used to report asset class performance: ASX S&P 200 Index, MSCI World Index ex Australia net AUD TR (composite of 50% hedged and 50% unhedged), FTSE EPRA/NAREIT Developed REITs Index Net TRI AUD Hedged, Bloomberg AusBond Composite 0 Yr Index, Barclays Global Aggregate ($A Hedged), Bloomberg AusBond Bank Bill Index, S&P ASX 300 A-REIT (Sector) TR Index AUD, S&P Global Infrastructure NR Index (AUD Hedged), CSI China Securities 300 TR in CN, Deutsche Borse DAX 30 Performance TR in EU. Hang Seng TR in HK, MSCI United Kingdom TR, Nikkei 225 in JP, S&P 500 TR in US.

General Advice Disclaimer

Any advice contained in this document is of a general nature only and does not take in to account the objectives, financial situation or needs of any particular person. Any decision to invest in products mentioned in this document should only be made after reviewing the relevant Product Disclosure Statements. Past performance is not a reliable indicator of future performance. Varria Pty Ltd is an authorised representative of Charter Financial Planning ABN 35 002 976 294 AFSL number 234665