February 2025: A new wave of concern hits equity markets

- Share markets were sold down over February as investors focused on concerns around the U.S. economy and tariff programs.

- Technology and growth stocks experienced the largest declines.

- A weakening in the U.S. economic growth outlook led to falls in bond yields.

International Equities

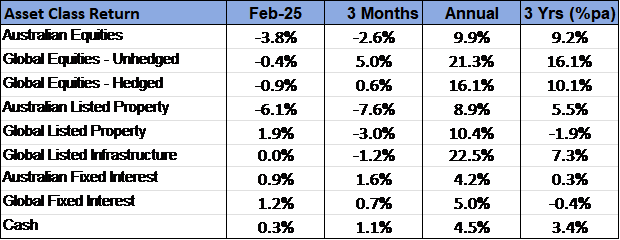

Following a bounce back January, global share markets finished in negative territory in February by an average of 0.9%. The U.S. technology sector led the market lower, with significant price declines recorded by Tesla (down 27.6%), Amazon (down 10.7%) and Alphabet (down 16.6%). The confirmation of the implementation of the U.S. tariff program, together with growing evidence of a slowing in U.S. economic growth, contributed to the weaker conditions on global equity markets. Generally, defensive sectors outperformed. More cyclical sectors, such as consumer discretionary, were sold off more heavily due to the lowering of economic growth forecasts.

Following a bounce back January, global share markets finished in negative territory in February by an average of 0.9%. The U.S. technology sector led the market lower, with significant price declines recorded by Tesla (down 27.6%), Amazon (down 10.7%) and Alphabet (down 16.6%). The confirmation of the implementation of the U.S. tariff program, together with growing evidence of a slowing in U.S. economic growth, contributed to the weaker conditions on global equity markets. Generally, defensive sectors outperformed. More cyclical sectors, such as consumer discretionary, were sold off more heavily due to the lowering of economic growth forecasts.

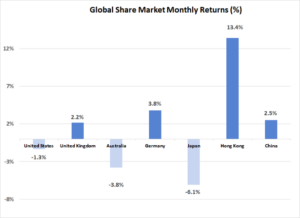

European markets performed better than the global average over February, with most Continental markets and the United Kingdom finishing the month in positive territory. A lower “growth” style component, as well as a new significant government spending program announced by the German Government, assisted European equities. Japan, however, experienced a sharp decline, with the Nikkei Index dropping 6.1%. a strengthening in the Japanese Yen, and expectations of higher interest rates, were negative influences on the Japanese share market last month.

February was a mixed month on emerging markets. There was some renewed support for Chinese equities, with the previous month’s revelation of Deep Seek’s artificial intelligence advances potentially attracting investors to the Chinese market. However, these gains were offset by another decline on the Indian market (down 7.1%), where valuations are viewed as being high relative to other markets. Taiwan (down 4.1%) also detracted, with some of the negative sentiment around the technology sector weighing on this market.

With bond yields in decline, real asset valuations held up well. Global listed property improved 1.9%, with infrastructure steady. Australian listed property, however, was an exception in falling 6.1%. The sector’s largest constituent, Goodman Group (down 14.1%), was also negatively impacted by the sell-off in the technology sector, given its heavy investment in data centres.

Australian Equities

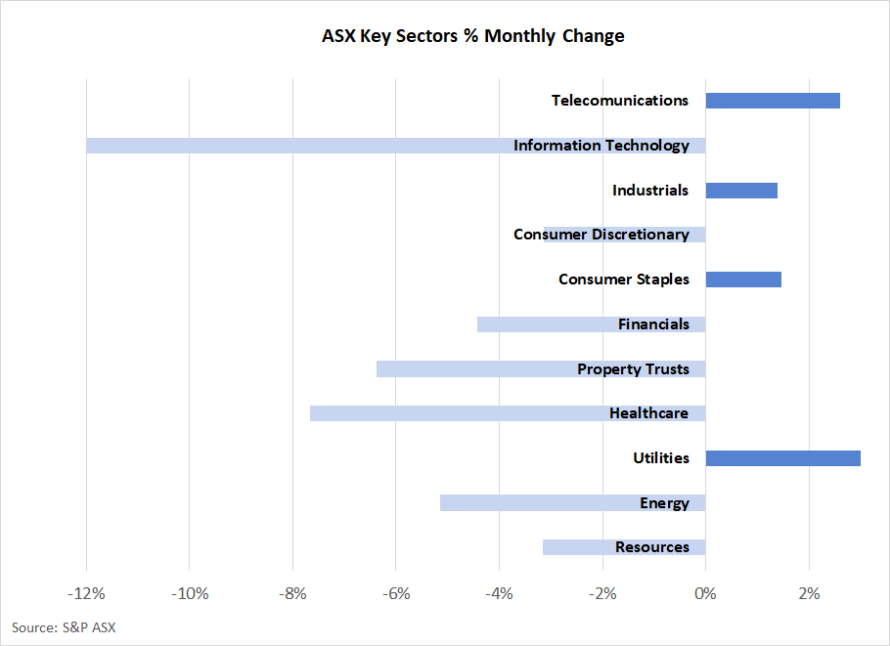

Australian equities underperformed over February, with the S&P ASX 200 Index falling 3.8%. The profit reporting season provided mixed result, with large falls being recorded by a range of stocks that missed earnings expectations. Although only providing a quarterly update, the National Australia Bank was a major contributor to the market decline, with the stock dropping 12.1% over the month.

Although there was a small appreciation in the iron ore price last month, the large mining companies lost ground. The largest declines, however, were recorded by the technology sector, which finished the month 12.3% lower. A combination of the broader global technology sector decline, and specific company announcements, saw stocks such as Wisetech (down 27.7%) and Block Inc (down 31.1%) sold down heavily.

Fixed Interest & Currencies

The trajectory of cash interest rates continued to be downwards. A 0.25% cut was announced by the European Central Bank in early March, following the 0.25% reduction in the Australian cash rate in mid-February. Australia’s cash interest rate now stands at 4.10%.

The trajectory of cash interest rates continued to be downwards. A 0.25% cut was announced by the European Central Bank in early March, following the 0.25% reduction in the Australian cash rate in mid-February. Australia’s cash interest rate now stands at 4.10%.

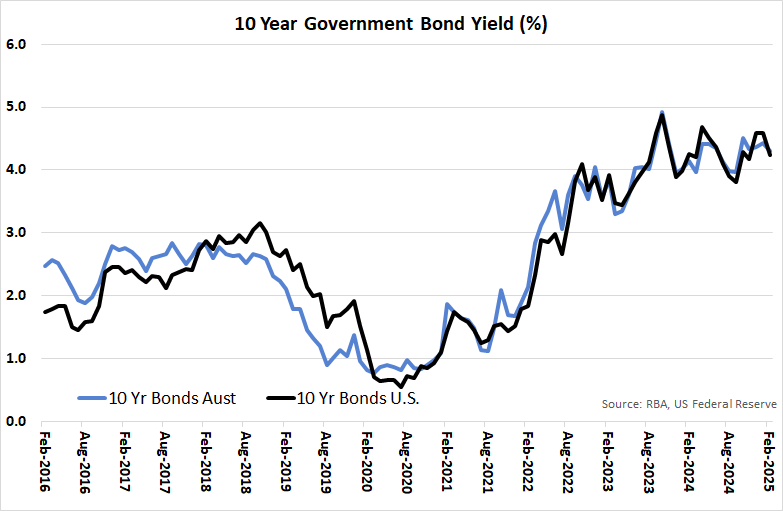

Softer than expected economic growth data in the U.S. saw declines in longer term interest rates as well. The U.S. 10-year Treasury Bond yield fell from 4.58% to 4.24% over the month. The Australian equivalent also declined, but not to the same extent, with the 10-year yield falling 0.13% to 4.30%. Stronger than expected employment data, combined with commentary from the RBA warning markets not to necessarily expect a series of cash rate reductions, may have limited the scope for longer term yields to decline in Australia.

As was the case in January, the $A remained relatively stable over February, with the currency just 0.2% lower against the $US at U.S. 62.1 cents. The $A was marginally weaker against the Euro as well; but did decline 3.3% against a strengthening Japanese Yen. A jump in Japanese inflation led to firming expectations of an interest rate increase there, which created additional support for the Japanese currency.

Outlook and Portfolio Positioning

Optimism has given way to concern as the dominant sentiment on global equity markets over recent weeks. The maintenance of buoyant investor confidence in a period of heightened geopolitical and policy uncertainty was always going to be a challenge after a period of strong share market growth. At the time of writing (11th March 2024), the United States S&P 500 Index has fallen 8.6% from its peak on the 20th February, with the market now trading at the same level it was in mid-September. As such, the post-election bounce on the U.S. share market has been fully reversed.

The share market correction has not been uniform across the globe, with European and the Chinese / Hong Kong markets holding up considerably better than the U.S. and Australia. At the epicentre of the price decline has been the U.S. technology sector, where the majority of the “Magnificent 7” stocks have experienced declines of more than 10% over the past month.

The catalyst for the sharp change in direction on share markets appears to be a combination of the following factors:

- The implementation of a program of tariffs by the U.S. Government on imports from Canada, Mexico and China, with retaliatory tariffs then announced by impacted nations. If maintained over the long term, tariffs are expected to reduce global trade and economic growth, as well as add to inflationary pressures. Although a tariff program was well flagged as being a central policy of the new U.S. administration, there was perhaps an underlying expectation on financial markets that a process of negotiation would result in the tariffs being significantly watered down or avoided.

- S. economic data over recent weeks has been weaker than expected, with evidence of softer consumer sentiment and spending, as well as a small decline in employment growth.

- In a recent media interview, the U.S. President, Mr. Trump, refused to rule out a U.S. recession this year.

Although the seriousness of the longer-term implications of the U.S. tariff program should be acknowledged, the recent spike in concerns over the possibility of a near term U.S. recession appear to be exaggerated. Despite some softening in growth momentum, economic conditions in the U.S. remain strong, with the most recent quarterly economic growth data showing an annual rate of expansion in excess of 2% in real terms. Unemployment remains low, corporate balance sheets are generally robust, and the financial sector is well positioned to continue to support growth via lending at interest rates now reduced due to the monetary policy easing that took place last year.

There also remains a likelihood that key elements of the tariff program will be temporary in nature, with their role as a negotiating tool being clearly apparent. Fundamentally, the Trump administration was elected as being supportive of economic growth and business profitability, and it is considered unlikely the administration will preside over a policy regime that does long lasting damage to the business sector. The new Government is expected to be highly motivated to ensure the equity market remains in a healthy state and a range of “business friendly” policy initiatives around tax cuts and deregulation are still anticipated. The recent sell-off on equity markets may increase the urgency and priority around the announcement and implementation of these policies.

History demonstrates very few examples of where specific government policies and geopolitical events have had long lasting impacts on share markets. Company earnings are ultimately what drive share market returns. There is little that has occurred over recent weeks that should be seen as changing the course of company earnings. The economic backdrop remains supportive, with the structural change driven by artificial intelligence applications still having a long runway in which to benefit shareholders and broader society. As such, the current correction appears to be sentiment, rather than fundamentally, driven. Changes in sentiment are inherently difficult to predict and the current mood may prevail for some time. However, periods of unjustifiably poor sentiment may also become the periods of best opportunities for investors.

Important Information

The following indexes are used to report asset class performance: ASX S&P 200 Index, MSCI World Index ex Australia net AUD TR, MSCI World ex Australia NR Hdg AUD, FTSE EPRA/NAREIT Developed REITs Index Net TRI AUD Hedged, Bloomberg AusBond Composite 0 Yr Index, Barclays Global Aggregate ($A Hedged), Bloomberg AusBond Bank Bill Index, S&P ASX 300 A-REIT (Sector) TR Index AUD, S&P Global Infrastructure NR Index (AUD Hedged), CSI China Securities 300 TR in CN, Deutsche Borse DAX 30 Performance TR in EU. Hang Seng TR in HKD, MSCI United Kingdom TR in GBP, Nikkei 225 in JPY, S&P 500 TR in USD.

General Advice Disclaimer

Any advice contained in this document is of a general nature only and does not take in to account the objectives, financial situation or needs of any particular person. Any decision to invest in products mentioned in this document should only be made after reviewing the relevant Product Disclosure Statements. Past performance is not a reliable indicator of future performance. Varria Pty Ltd is an authorised representative of Charter Financial Planning ABN 35 002 976 294 AFSL number 234665