March 2025: US Tariffs Trigger Further Share Market Losses

- For the second consecutive month, share markets were sold down in response to developments around the U.S. tariff program.

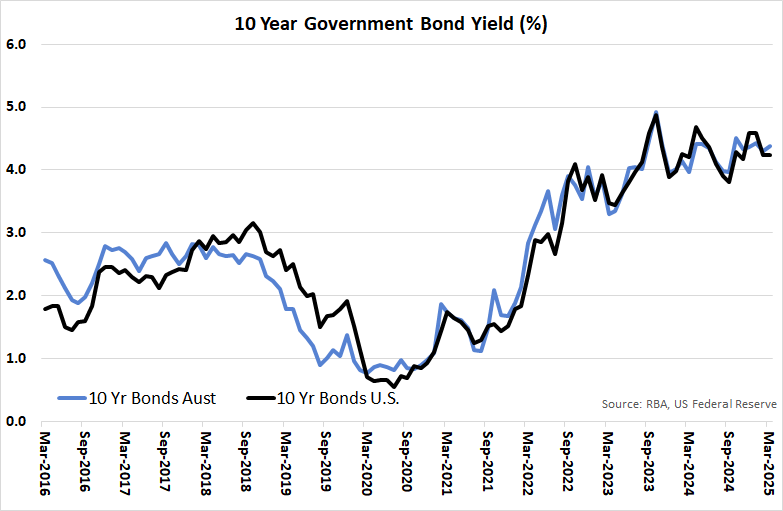

- Bond yields were relatively stable in March, after declining in late February.

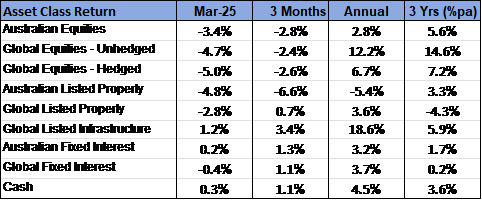

- Defensive and interest rate sensitive equities outperformed, with infrastructure the only positive growth asset class in March.

International Equities

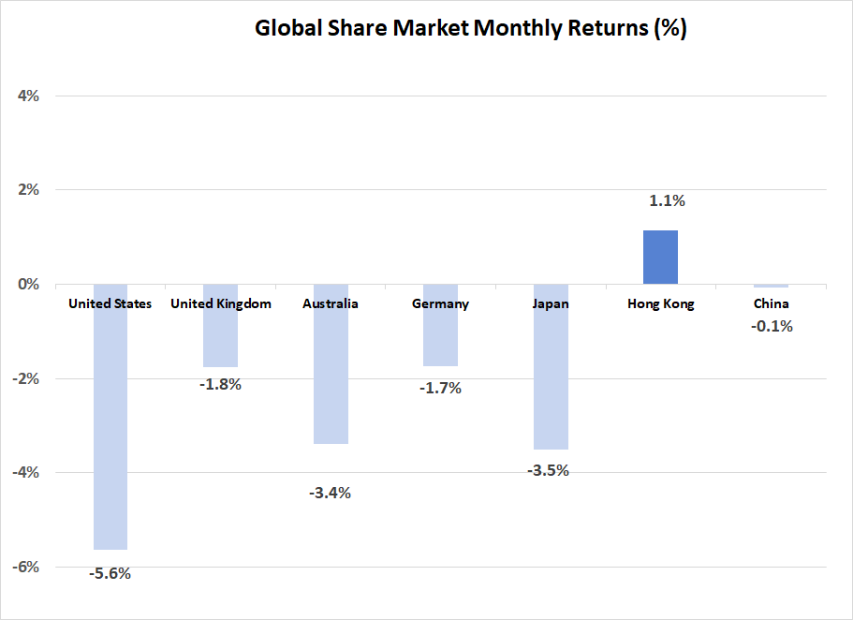

Concerns over the growing U.S. tariff program, and the negative impact this may have on economic growth, continued to weigh heavily on share markets over March. The majority of the reduction took place early in the month, with a continuation of the pattern set in late February. However, after stabilising mid-month, there was another step down late in March ahead of the “Liberation Day” tariff announcements on April 2nd. With much of the concern being centred around the impact of tariffs on the U.S. economy, the U.S. share market led global markets lower with the S&P 500 Index falling 5.6% over the month. As was the case in February, there were significant losses across the large U.S. technology sector, with Amazon, Tesla, Nvidia and Meta all recording drawdowns of more than 10% for the month. Defensive stocks on the U.S. market performed materially better than average, with minimal losses in the healthcare, utilities and consumer staples sectors. In contrast, smaller companies were sold down more heavily, as was the consumer discretionary sector, which dropped in value by 9.5%.

Although posting small negative returns, European markets performed relatively well. Hopes that a German government announcement of a new spending program (heavily orientated towards defence) will be the start of a greater willingness by European authorities to use fiscal stimulus, helped support European markets last month. Additionally, the European share market is generally regarded as being cheaper, more defensive, and more “value” orientated in style than the U.S., all factors which generally provide support in a period of equity market weakness.

Similarly, the Chinese share market was also buoyed by a government announcement indicating a renewed commitment to supporting domestic growth and consumer spending. Overall, the Chinese market was flat for the month. This enabled the MSCI Emerging Market Index to finish March in slightly positive territory, with gains recorded in Eastern Europe and South America, in addition to a 6.9% bounce back on the Indian market. Taiwan, however, stood out with a 10.5% decline, which reflected the broader negative sentiment attached to the technology sector last month.

Global real assets generally held up well. Infrastructure benefited from an ongoing shift to defensive sectors and gained 1.2%. With an annual return of 18.6%, infrastructure is now the top performing asset class on a 12-month basis. Global listed property was 2.8% lower in March but remains 0.7% higher for the quarter. In contrast, Australian listed property declined 4.8% last month, with the largest constituent and data centre specialist, Goodman Group, leading the sector lower with a decline of 9.2%.

Australian Equities

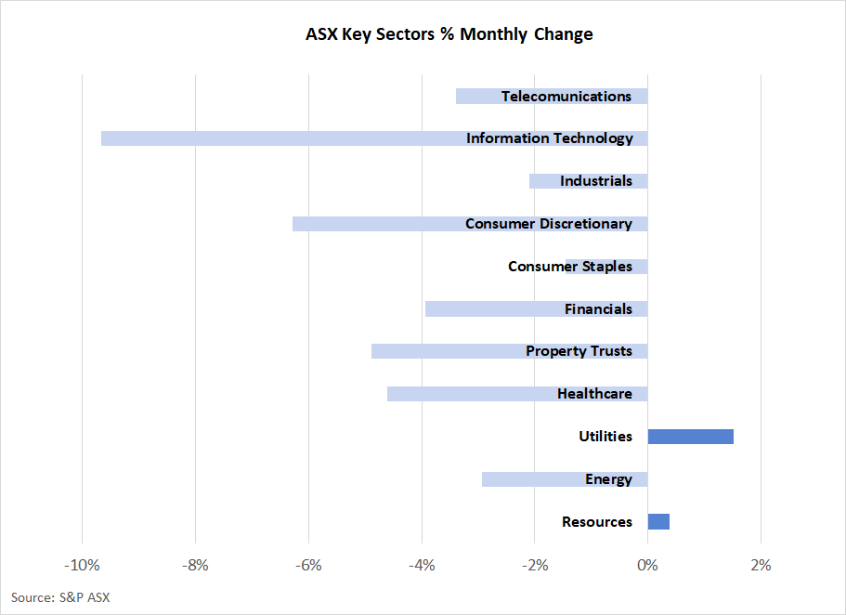

Australian equities performed slightly better than the global average over March, with the S&P ASX 200 Index falling 3.4%. The pattern of price movement across sectors was similar to that prevailing on the U.S. market, with technology and consumer discretionary being the weakest sectors.

The more defensive sectors had more support over the month, as did the resource sector, which gained 0.4%. More positive sentiment around the outlook for the Chinese economy may have contributed to this gain in resources, which came despite a 4.1% reduction in the iron ore price over the month. Rio Tinto was a standout with a 5.0% increase for the month.

Fixed Interest & Currencies

There was minimal movement in interest rates across the globe last month, either at the front end or long end of the yield curve. Although longer term bond yields declined in late February in response to a lowering in U.S. growth expectations, this trend didn’t continue through March, despite the ongoing concerns expressed on equity markets.

Possibly, the inflationary impact of the tariff program has weighed on bond markets, as the expected pick-up in U.S. inflation will reduce the scope for the U.S. Federal Reserve to cut interest rates in the near term. U.S. 10-year Treasury Bonds finished March virtually unchanged at 4.23%, with the Australian equivalent 10-year yield rising 0.08% to 4.38%.

The Australian dollar continued to remain relatively stable, despite its historical tendency to decline in periods of weaker equity markets. Against the U.S. dollar the $A firmed from U.S. 62.1 cents to U.S. 62.8 cents. However, the $A was 3.1% weaker against the Euro, but stable against the Japanese Yen.

Outlook and Portfolio Positioning

Although the use of tariffs by the new U.S. administration was well telegraphed, the magnitude and breadth of the program is greater than the share market consensus had anticipated. As it stands, the U.S. is set to experience an average tariff rate of approximately 25% on all goods imported, with varying rates applying depending upon goods type and country of origin. The recent news that China have in turned retaliated, with plans to impose a 34% tariff on all goods imported from the U.S., takes the seriousness of the trade restrictions to another level, and opens up the prospect of further escalation.

The negative share market response to the escalation in tariffs has been significant, with global equity markets falling approximately 15% between mid-February and early April. The unique nature of recent events does make it difficult to judge what the exact investment response should be. We may be approaching the end of the period of negative news flow associated with the new tariff regime. Negotiations, logic and ultimately self interest may lead to a more moderate path for the tariff program. If this is the case, share market valuations could potentially snap back upwards very quickly. However, as we have seen with share market corrections in the past, it often takes valuations to fall to excessively cheap levels before buyers can be enticed back. As such, it may be too early to aggressively lift equity allocations, despite valuations becoming attractive at face value.

Whilst it may be too early to embark on a significant rise in overall share market allocations, any plans to adjust portfolio positions should be seeking to take advantage of assets that may have been sold down as part of the broader market trend but are fundamentally less likely to have been damaged by the new tariff regime.

Arguably, the Australian share market stands out as one market where valuations have become materially cheaper, despite a relatively low direct impact from the tariff program. Some Australian exporters will now have a relative advantage over others in exporting to the U.S.; and Australian companies are now in a better to position to compete with U.S. producers in selling to the Chinese market. With the cash interest rate higher in Australia than most other developed economies, and the government budget deficit lower, there is also potentially more scope for policy easing here than elsewhere – should some form of domestic policy stimulus be required.

Australia’s outlook now contrasts starkly to that of the U.S., where U.S. consumer spending will be constrained by tariff induced price increases. Policy stimulus in the U.S. will be difficult due to the constraints on monetary policy caused by the inflationary tariffs, as well as the acknowledged need to reduce their government budget deficit, rather than embark upon stimulatory spending. This comparison of the state of the U.S. and Australian economies has implications for the potential relative returns on bond, equity, and currency markets.

Notwithstanding some opportunities that may have emerged for portfolio adjustments over recent weeks, the tariff program, and the U.S. policy regime more broadly, has made investing more complex and outcomes more uncertain. In this environment, diversification and professional active management of portfolios is of paramount importance. As such, the recipe for investment success may be somewhat different to that which has prevailed for most of the past two years when passive U.S. dominated index strategies have been difficult to beat.

Important Information

The following indexes are used to report asset class performance: ASX S&P 200 Index, MSCI World Index ex Australia net AUD TR, MSCI World ex Australia NR Hdg AUD, FTSE EPRA/NAREIT Developed REITs Index Net TRI AUD Hedged, Bloomberg AusBond Composite 0 Yr Index, Barclays Global Aggregate ($A Hedged), Bloomberg AusBond Bank Bill Index, S&P ASX 300 A-REIT (Sector) TR Index AUD, S&P Global Infrastructure NR Index (AUD Hedged), CSI China Securities 300 TR in CN, Deutsche Borse DAX 30 Performance TR in EU. Hang Seng TR in HKD, MSCI United Kingdom TR in GBP, Nikkei 225 in JPY, S&P 500 TR in USD.

General Advice Disclaimer

Any advice contained in this document is of a general nature only and does not take in to account the objectives, financial situation or needs of any particular person. Any decision to invest in products mentioned in this document should only be made after reviewing the relevant Product Disclosure Statements. Past performance is not a reliable indicator of future performance. Varria Pty Ltd is an authorised representative of Charter Financial Planning ABN 35 002 976 294 AFSL number 234665